2023-07-19 Japan retail > China retail

Continuing to dive into Japan ideas. As 2Q23 results season rolls in, I notice the divergence - Japan results beats and revise up guidance, while the flat or less confidence for China consumer cos.

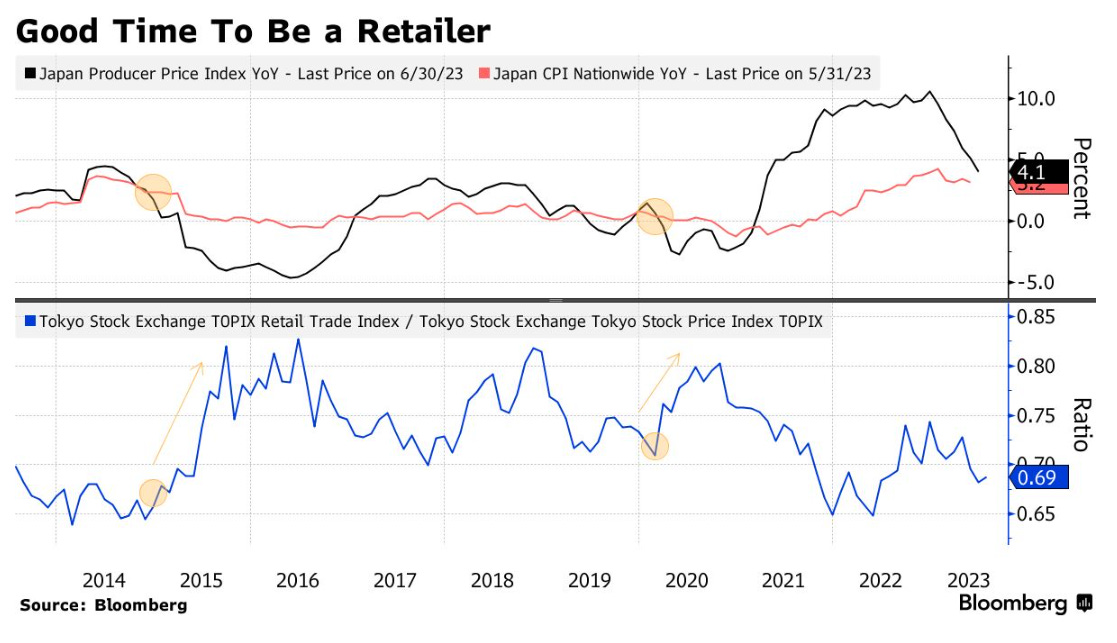

RY: Start of 2Q23 results season, I can't help but notice that divergence in consumer sector performance in China vs Japan. Chinese consumer companies (i.e. Anta) showing wavering confidence amidst weaker sales trend due to weaker physical store sales in higher-tier cities. Meanwhile, Japan consumer names - Lawsons, Uniqlo, 7-11, are are showing Japan-domestic sales grow strong and beating mgmt expectations. Research report shows a CPI > PPI trend signals strong retail stock performance, so this should be positive for Japanese consumer companies. On the flip side, strategists warn that foreign buying of Japan is done and recommend a pull back before a summer lull. The jury is still out on Japan's near term direction, but it seems like funds already in position are comfortable on the outlook (i.e. corporate reform materializing).

[BBG] China Growth Risks Hurt Asia Stocks; Yen Lower: Markets Wrap. The yen weakened for a second day following Bank of Japan Governor Kazuo Ueda’s comment that it would maintain monetary easing unless there is a shift in its price goal view. BOJ is unlikely to alter its monetary policy in next week’s meeting, said Shoki Omori, chief desk strategist at Mizuho Securities. [RY: JPY at 139]

[BBG] UBS Wealth Arm Looks for Pullback in Japan Stocks Before Buying. UBS advise to wait for 5-8% correction before buying. Notes that valuation is no longer depressed and share buyback news will be muted during summer.

[GS] Japan Technology: Hardware - Industrial Electronics: Asian investor feedback: Restructuring expectations remain; focus gradually shifting to execution. UBS says Asian investors are bullish on Japanese equities and expectation on restructuring remains high, but moving from discussing restructuring plans to likelihood of their execution. Names include: Hitachi, Panasonic Holdings and Mitsubishi Electric, and Fujikura and Fuji Electric.

[BBG] Inflation Proves Blessing in Disguise for Japan Retailers. "retailers appear to be passing on rising costs more than investors have been expecting,” and that’s supporting the stock". Lawsons Raise Chicken Nugget Prices for First Time in 36 Years in April 2022 by 10% to JPY238. Some strategists and fund managers are rotating their stock-selection to favor domestic demand-driven ones. Analysts’ earnings forecasts have been steadily improving for the sector. The 12-month forward EPS for the TSE Retail Index has risen 7.1% so far this year, much more than 2% increase for the Topix Index. Yet TSE retail gauge has also underperformed the broader Topix so far this year amid other opportunities such as semiconductor-related firms, trading houses and shares with low price-to-book ratios. Wholesale price inflation, a proxy of cost increases for retailers, “looks set to fall below consumer price inflation within a couple of months,” and when that happens, retailer stocks tend to outperform

[GS] Sportswear - Updating the industry model and 1H23 Preview. 1) outlook on discount improvement given weaker consumption power, 2) initial July-Aug trading, 3) long-term sales growth outlook (Li Ning earlier lowered the target from >20% to high teen; Anta will host an Investor Day in October to update the outlook), 4) risks in higher A&P to drive stronger sales growth), 5) pricing trend and mix changes.

[GS] Anta Sports Products (2020.HK): 2Q23 operational update: in-line with the lowered expectation; confident on margins; Buy. maintained the guidance of DD growth for both Anta brand and Fila, though the tone didn't sound encouraging as they also observed weaker trend from May into early July. higher marketing expenses in 2H23 to advance the 2024 Paris Olympics related marketing campaigns from 2H23. revise down our 2023-26E earnings estimates for Anta by 1-11% to factor in slower sales CAGR and operating leverage going forward

[Citi] Anta (2020) In-line 2Q23 retail sales vs market’s high earning expectations. Fila‘s significant divergence of weak offline sales (up by merely LSD to MSD) vs strong online sales (up 60-65% YoY) in 2Q23, Fila‘s recovery was largely driven by new penetration into low-tier cities (via livestreaming platforms), rather than improved products or branding, in our view. Mgt admitted that its retail sales have been below mgt’s expectation on slower-than-expected volume (albeit resilient ASP) since May and its internal sales target completion rate dropped from 100%+ in Jan-April to 90%+ in May-July.

[GS] Lawson (2651.T) Earnings Review: Above expectations; 1Q shows earnings clearly on recovery path but this looks priced in; Neutral - 12 July.

Based on 1Q earnings, we revise up our FY2/24-2/26 operating profit estimates by 12%/15%/14%

[MS] Lawson (2651) F2/24 1Q Results: Smooth Start - 11 July. Changes in accounting may have led to results straying further from consensus than usual and the timing of SG&A expenditures was pushed back. (the Refinitiv consensus OP figure, which factored in a mix of JGAAP- and IFRS-based forecasts, was ¥15.5bn; we estimate the prior buy-side average IFRS-based forecast at around ¥16-17bn). after discounting the technical effects associated with the application of IFRS the contribution was only about +¥1bn). key indicator for domestic convenience store business, SS sales growth, was +6.2% (vs the company's full-year target of +4.0%), and the gross profit margin was 31.3% (+0.5ppt YoY, reflecting margin improvement in food subcategories and a lower weighting of tobacco sales).

[MS] Fast Retailing (9983) F8/23 3Q Results: Full-year OP Guidance Raised on China Strength - July 13, 2023. 3Q OP of ¥110.3bn (+34.8% YoY) beat consensus by 7.7%. The company raised its F8/23 OP forecast by 2.8% to ¥370bn (+24.4% YoY, 1.9% above consensus) mainly due to strength in Greater China. Same-store sales growth in Mainland China exceeded 40%. Sales beat the company's plan against a backdrop of consumption recovery timing coinciding with rising temperatures, and reinforced branding. Inventories that had been excessive through last year also normalized. Domestic Uniqlo -5.7% YoY. Sales beat the plan, but GPM worsened by 1.7pt YoY due to yen depreciation and inventory disposal (a slightly larger drop than planned), leaving OP short of plan. Rising salary levels contributed to a 0.3pt uptick YoY for the SG&A cost ratio (improved relative to the plan).

[FT] Uniqlo owner raises annual forecast after surge in post-pandemic China sales. “From our viewpoint, China’s consumption seems to be recovering strongly and we were able to reaffirm that demand is strong for our low-priced daily clothing.”

[MS] Seven & i Holdings (3382) F2/24 1Q Results: US Gasoline C/G Declines; OP -5.5% behind Plan - July 13, 2023.

Seven & i reported F2/24 1Q OP down -19.9% YoY to ¥81.9bn, -5.5% below guidance and -19.2% below consensus. With the recording of a transfer-related loss of ¥4.8bn on the sale of Barneys Japan, NP came in -13.9% below plan. Domestic convenience store business +8.1% YoY, +5.1% above plan. The company was successful in bolstering original merchandise. SS sales were up +4.9% and the gross margin on merchandise improved by +0.4ppt. US convenience store business -52.3% YoY, -42.0% below plan. Gasoline c/g dropped off the historic highs recorded in the previous year

[MS] Bic Camera (3048) - F8/23 3Q Results: Brisk Inbound Demand Cannot Cover Slumps in White Goods and TV - July 11, 2023. Bic reported F8/23 3Q OP down -39.7% YoY to ¥3.5bn, falling short of guidance (¥5.1bn), consensus (¥5.6bn), and our forecast (¥4.2bn). Sales: Inbound sales were brisk but this was not enough to make up for slumps in white goods and TVs. Gross profit margin: GPM was -0.4ppt below plan on a consolidated basis (parent -0.6ppt, Kojima +0.2ppt). The sales mix deteriorated as low-margin video game sales were stronger than anticipated while high-margin white goods sales slumped. As people start to move around outside their homes again, household spending on eating and drinking and on services is rising, but purchases of durable goods are lackluster.

[BBG] China AI Chip Firm Targeting Nvidia Seeks HK IPO in 2023. 壁仞科技 GPU maker. To raise about 2 billion yuan ($279 million), Last year raised funds at valuation of 17 billion yuan ($2.4 billion). investors including IDG Capital, Ping An Insurance Group Co. and China Merchants Capital

[Reuters] CLSA will relocate staff to mainland. plans to move dozens of bankers from its offshore platform CLSA in Hong Kong to the mainland to cut costs and meet Beijing's call to bridge income inequality

[BBG] Tencent slumps as chips feel the heat. Prosus said earlier that the Amsterdam-listed firm would continue to cut its holdings in the company by up to three percentage points a year and expects the stake to drop to 24 to 25 percent by the year-end from the current 26 percent.

[TheStreet] Hedge Fund Manager Doug Kass Predicted This Year's Rally: Here's What He Thinks About the Rest of 2023. "The S&P dividend yield is only 1.50% compared to the yield on the one-year Treasury note of 5.40% - that's the largest gap in decades, he is bearish on 2H23 as equities are overpriced relative to interest rates. Notes PE of S&P (ex tech/AI) is 18x, above 16x average of the last 5 decades, and believes EPS forecasts needs to be meaningfully upward revised to produce positive returns.